Attached: 4 images

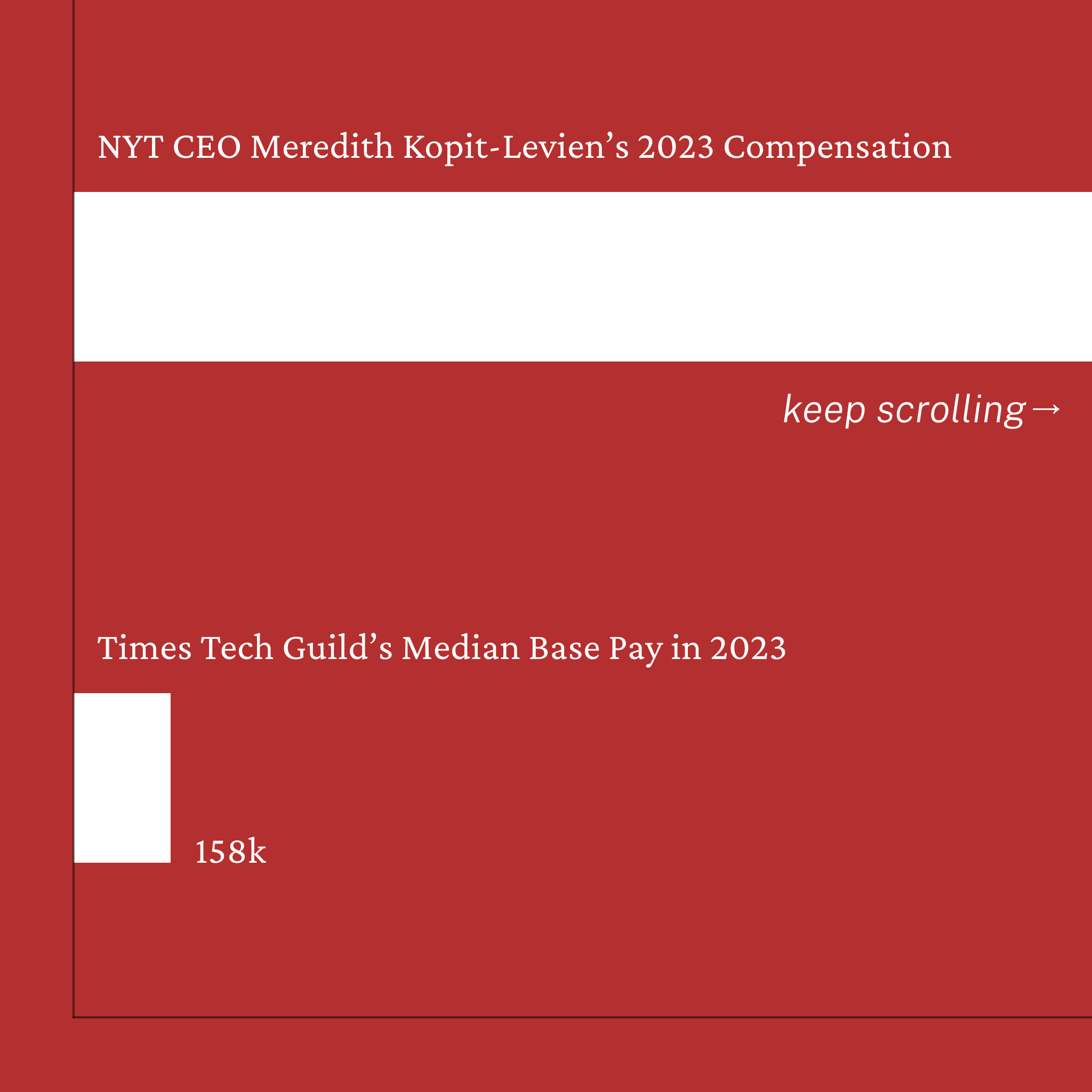

The New York Times Company made $2.4 billion in revenue in 2023, and our CEO gave herself a 36% raise, while members of our unit were given around 3% with persistent wage gaps for women and people of color.

#ReadyToStrike #Union #Unions #Tech #Election #Election2024 #Labor #Strike #CollectiveBargaining #Contract #NewsGuild #CWA #Solidarity

Exactly. If you’re not a founder, you’re an employee, and you’ll need to earn your keep.

I think CEOs should be paid almost exclusively in stock, but that stock should also be taxed as regular income. If you’re regularly hopping, you won’t have enough time to get a meaningful amount of stock, so your income would be fairly low.

Stock — at least, RSUs — is AFAIK taxed like supplemental income ( https://www.harnesswealth.com/articles/what-you-need-to-know-about-restricted-stock-units-rsus/ ), which is very similar to regular income. Stock options are different though, and maybe this is what you’re referring to — I think (???) options can be beneficial to the recipient from a tax perspective vs. other compensation but not an expert…

And then there are capital gains, which is a different, but related, story…

Huh, I thought there was something like RSUs that were delayed compensation, but that’s apparently wrong. Looking into it, it looks like they don’t really avoid taxation on the actual compensation (either they’re taxed on vesting for RSUs, or taxed on the option spread), and one of the main benefits is delayed taxation/rolling options if the value drops.

So the main loophole seems to be inheritance taxes, which is unrelated to compensation, but does fuel the trend of borrowing instead of selling assets. If the estate was taxed for all unrealized capital gains before inheritance, I think we’d see a lot higher income tax bills from execs because it would essentially eliminate the “borrow/buy/die” loophole. We could take it one step further and require immediate taxation anytime stock changes hands (so even charitable giving would trigger capital gains tax).

Exactly. If you’re not a founder, you’re an employee, and you’ll need to earn your keep.

I think CEOs should be paid almost exclusively in stock, but that stock should also be taxed as regular income. If you’re regularly hopping, you won’t have enough time to get a meaningful amount of stock, so your income would be fairly low.

Stock — at least, RSUs — is AFAIK taxed like supplemental income ( https://www.harnesswealth.com/articles/what-you-need-to-know-about-restricted-stock-units-rsus/ ), which is very similar to regular income. Stock options are different though, and maybe this is what you’re referring to — I think (???) options can be beneficial to the recipient from a tax perspective vs. other compensation but not an expert…

And then there are capital gains, which is a different, but related, story…

Huh, I thought there was something like RSUs that were delayed compensation, but that’s apparently wrong. Looking into it, it looks like they don’t really avoid taxation on the actual compensation (either they’re taxed on vesting for RSUs, or taxed on the option spread), and one of the main benefits is delayed taxation/rolling options if the value drops.

So the main loophole seems to be inheritance taxes, which is unrelated to compensation, but does fuel the trend of borrowing instead of selling assets. If the estate was taxed for all unrealized capital gains before inheritance, I think we’d see a lot higher income tax bills from execs because it would essentially eliminate the “borrow/buy/die” loophole. We could take it one step further and require immediate taxation anytime stock changes hands (so even charitable giving would trigger capital gains tax).